DON’T TRADE THE MARKET ALONE

Sign Up for a Free Test Drive

Of our products and services

STEP 1: Education

Becoming a successful day trader is no easy task. It’s important to make sure you are prepared before diving into the markets. At Investors Underground, we provide top-notch education that allows you to learn from our mistakes and increase your chances of profitability.

STEP 2: Brokers and Tools

In order to be successful in the stock market, you need to make sure you have access to the proper tools. Brokers are one of the most important parts of your trading, so it’s important to choose one that will maximize your trading. Here are a few of our favorites.

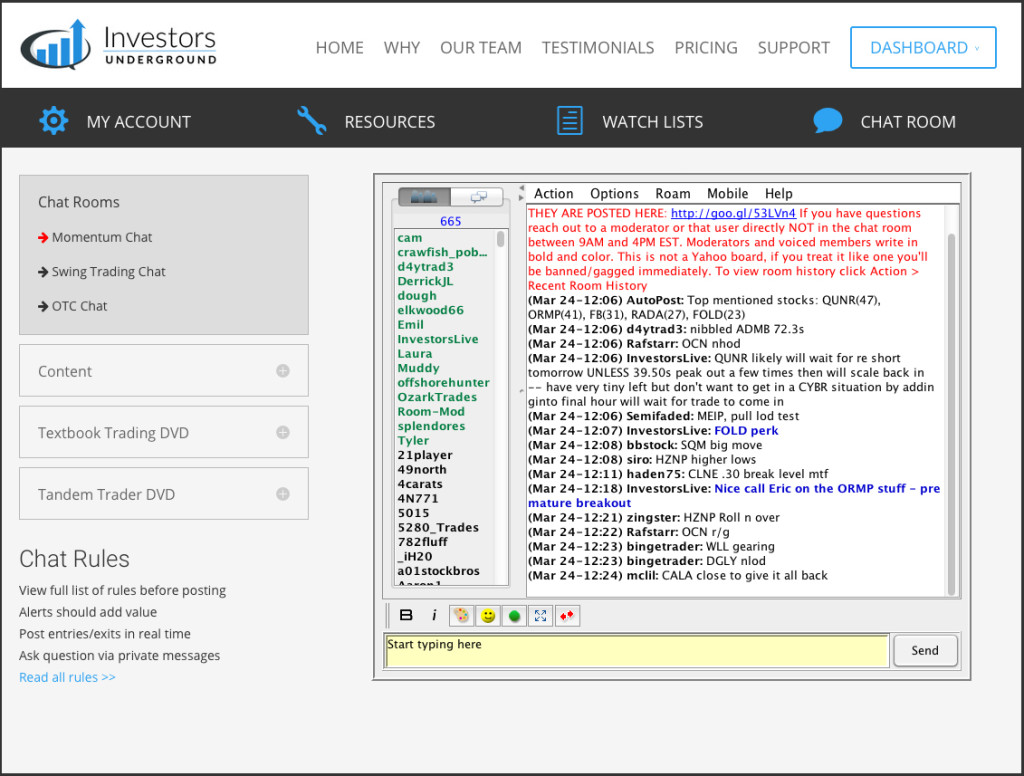

STEP 3: Live Chat

Day trading is a non-stop learning experience. You need to surround yourself with a community that will help you succeed. Investors Underground chat is designed to provide traders with actionable alerts. We also have a team of moderators ready to help answer your questions